Double materiality is not a mystery

What is assessed and how?

Regulation provides the framework for the assessment - the target and the method

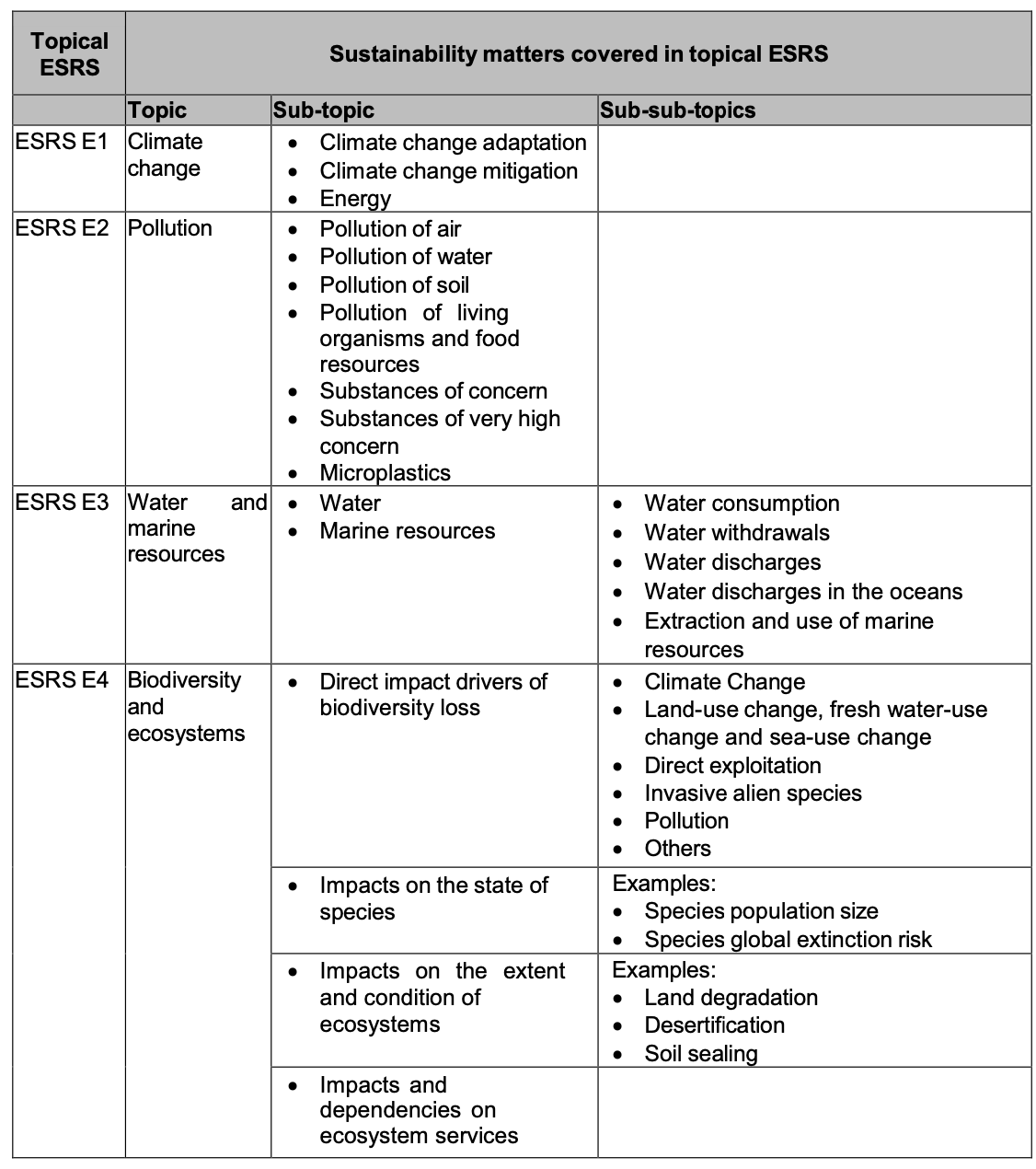

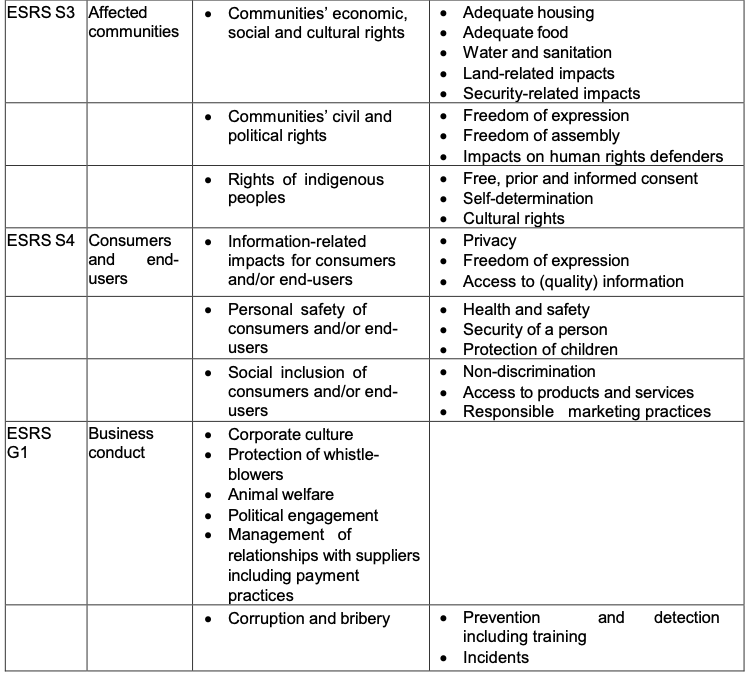

When conducting the double materiality assessment the target should be the sustainability topics listed in ESRS 1: AR16. The topic list is provided below.

ESRS 1: chapter 3 tells how the double materiality should be conducted. First the impacts that to company has to the 92 topics (impact materiality) and the impacts that these 92 have on the company (financial materiality), should be mapped. After this the materiality of the impacts is defined using the method provided by the regulation.

Below is a diagram of how the materiality assessment should be conducted according to the regulation.

To get the result, mathematical parameters can be given to the different aspects of materiality and a threshold for materiality can be set. E.g. 5 for scale, 5 for scope, 5 for remediability, these are added and if the value is 8 or above the topic is material. These numerical values can be acquired using company data - costs and sales and the sustainability impacts created by the sectors that make up the costs and sales.

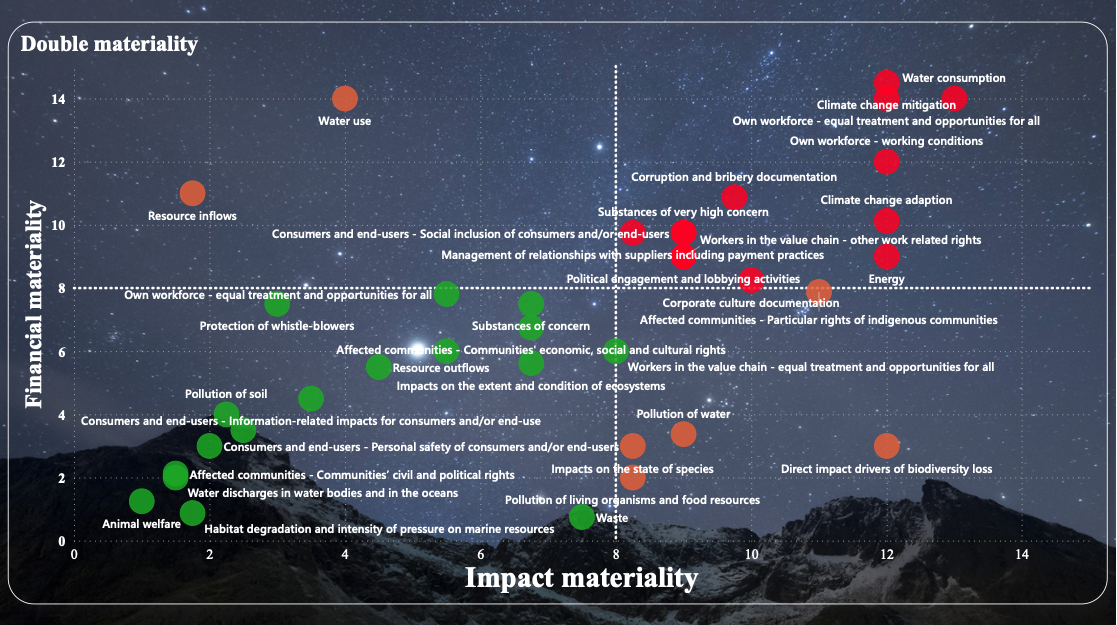

We have developed an automic tool that can be used to conduct the double materiality assessment. The requirements of the regulation (the target and the method) are built in to the tool. This means that the client can conduct the double materiality assessment with the tool and automatically get the results and the documentation required for assurance. The largest companies in Finland have used the tool to get the results of the double materiality assessment. Pictures from the results are at the end of the page.

We need your consent to load the translations

We use a third-party service to translate the website content that may collect data about your activity. Please review the details in the privacy policy and accept the service to view the translations.